Estimated read time: 7 minutes

I’ve been thinking a lot about how I became a “late bloomer” in some areas of life—but not when it came to money. These money tips for 20s and 30s helped me begin building wealth early, and they might just help you too. I took the advice of the men in my life: my dad (even though our relationship isn’t always easy), my grandpa, my godfather, and my close friend Steven. Their wisdom shaped how I approached money from my 20s onward.

In this post, I’m sharing the exact lessons I follow that have kept me from being a financial late bloomer—and how you can apply them too.

1. Start Early: Your 20s Are the Golden Years for Wealth Building

My dad always told me to start contributing to retirement as soon as I could. So, at 25, I began putting money into my 401k/403b—and I always contributed at least the amount my employer matched (7% at my job).

One thing I wish more people understood: 401k/403b contributions come out before taxes, so the hit to your paycheck is smaller than it seems. While it might feel good in the short term to keep that money in your pocket, even starting with small contributions can make a BIG difference over time. And because it’s pre-tax, you’re saving more than you’re actually missing in take-home pay.

This simple move—just contributing consistently over time—put me on the path to financial security. The earlier you start, the more time your money has to grow.

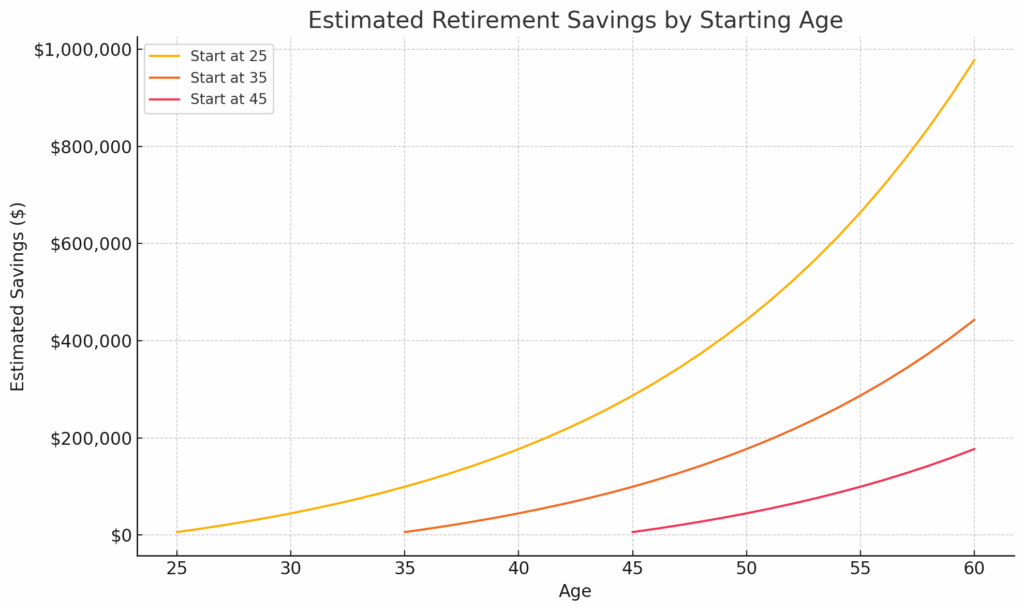

Here’s the math:

This chart shows how contributing $500 per month can grow your savings over time, depending on when you start.

It’s not about having a lot of money to invest—it’s about starting as early as you can and letting time do the heavy lifting. Set it and forget it.

2. Live Below Your Means (Even if It’s Uncomfortable for a Little While)

My grandpa taught me to live below my means—and I developed my own simple formulas based on his advice:

- Car: No more than 1/3 of your annual salary.

- House: No more than 3x your annual salary—but if you’re buying a condo or townhome, I recommend 2x to leave room for HOA fees.

- Rent + Utility Bills: Should be 50% or less of your monthly income—even if that means living in an older apartment, a less trendy neighborhood, somewhere without a ton of amenities, or having a roommate.

These aren’t hard rules, but they helped me stay on track when it came to big financial decisions.

In 2018, I was earning $55,000/year and living in a small apartment in Memphis, Tennessee. While I was financially comfortable—paying my bills, saving, and avoiding new debt—the environment started to take a toll. My neighborhood felt increasingly unsafe, and the apartment itself was making me sick.

That discomfort became a catalyst for growth. I realized that if I wanted a better quality of life, I needed to increase my income. So, in 2020, I went for a promotion and started a remote job. In 2021, I moved to Texas for a better apartment and a fresh start. By 2022, I had earned another promotion—and in 2025, at the age of 32, I just bought my first home.

For context, the average age of first-time homebuyers in the U.S. is 38 (2024 data)—so buying at 32, and most importantly within my budget, has put me ahead of the curve.

3. Avoid Lifestyle Creep (Steven’s Wisdom)

Steven told me early on: Just because your salary increases doesn’t mean you should immediately increase your lifestyle. I took that advice to heart.

From 25 to 32, I proudly drove the same vehicle—my Jeep Renegade aka Baby Blue. I didn’t upgrade my car, move to a luxury apartment, or suddenly start splurging just because I had a little more money.

Instead, I used that time of financial stability to invest in myself:

- I went on a few vacations.

- I updated my wardrobe to feel more confident.

- I got Invisalign to improve my smile.

- I went back to therapy.

- I got a gym membership.

- And I launched Late Bloomer Chronicles—a blog that turned into a passion project, helping me grow both personally and professionally.

All of these were intentional choices that contributed to my physical, mental, and creative blooming—without derailing my financial goals.

Avoiding lifestyle creep doesn’t mean you can’t enjoy life. It means making smart, purposeful upgrades that align with your long-term vision—not just spending more because you can.

4. Use Credit Cards Like Debit Cards

Steven also taught me to treat my credit card like a debit card. I only spend what I can afford to pay off in full every month. That approach helped me build excellent credit without falling into debt traps.

For context: In 2018, when I started my first “big girl” job, my credit score was embarrassingly low—in the 500s. I didn’t fully understand how credit worked, and like many people, I had made a few missteps. But five years later, by sticking to this simple habit of only spending what I could pay off—I crossed the 750+ credit score mark.

And I’m intentional about the cards I use. For example, I use an airline credit card for my everyday purchases, and I haven’t paid for a flight in cash since 2022. #FreeFlights

5. Save Up, Don’t Finance (Unless It’s for a Home)

I don’t believe in buy-now-pay-later schemes or financing things like furniture, clothes, or vacations. If I couldn’t afford it, I’d either save up or hustle—working extra hours or picking up a side job.

One of my favorite Steven tips:

“Work part-time in the places you spend the most money.“

For me, that meant working at The Gap every summer during my undergraduate years. The 50% employee discount helped me upgrade my wardrobe without going broke (and I believe they still offer that discount today).

Also—don’t sleep on Facebook Marketplace. It’s full of secondhand gems from people who already spent full price so you don’t have to. Use your negotiating skills and let someone else take the financial L while you furnish your space for half the cost.

If you’re into fashion, why not work at your favorite clothing store? If you love books, work at a bookstore. The point is: get creative and let your spending habits fund themselves—without swiping a credit card or financing every purchase.

6. Avoid the Get-Rich-Quick Traps

In the words of my Godfather, who is a millionaire, salesman, entrepreneur, and voice of reason:

“There’s no such thing as getting rich quick without risking everything. If someone is selling you a shortcut—especially one that involves recruiting others into a program so they can make money—it’s probably a Ponzi scheme or a multi-level marketing (MLM) company.”

I learned early on to steer clear of anything that promises overnight wealth. If you want to build something—a blog, a fashion brand, a photography business, rental properties, or flipped homes—do it the old-fashioned way:

- Use your own money.

- Build your influence over time.

- Acquire the skills needed to create your business—take a class, write, take photos, edit content, LEARN. NEW. THINGS.

- Focus on serving real customers, not recruiting friends and family into your downline.

- Find a mentor AND listen to people who are actually accomplished.

You’ll have a stronger foundation, more control, and a better chance at long-term success. Plus, you get to write it off on your taxes. #RefundCheck

7. Book Recommendation: Everyday Millionaires

If you want to go deeper, I highly recommend the book Everyday Millionaires. It’s full of stories and data showing that ordinary people—not lottery winners or celebrities—become millionaires through smart, steady habits.

Final Thoughts

It’s easy to feel behind when you see others living flashy lifestyles. But real wealth? It’s quiet. It’s built over time.

Your 20s to 40s are a golden window to lay a solid financial foundation—but it’s never too late to start. These money tips for 20s and 30s helped me to avoid becoming a financial late bloomer, and they can help you build the life you want too.

So take what works for you, make it your own, and remember: your wealth journey doesn’t have to look like anyone else’s. Just start.

Until next time,

Later Bloomers 🌸

Want to learn more about self-growth? Read my post on how I overcame body dysmorphia through mirror exposure therapy.